Mortgage defines any loan which is secured by real estate. It can be divided into “Residential Mortgage” and “Commercial Mortgage” based on the type of real estate the loan is secured by.

- Residential Mortgage is a loan that is secured by a residential property such as condominium, townhouse, detached house, etc. Residential Mortgage is used to purchase a residential real estate, renovate existing residential property or to acquire additional funds for personal use.

- Commercial Mortgage is a loan that is secured by a commercial property such as office building, shopping center, retail plaza or industrial warehouse, etc.

For residential mortgage, maximum limit to borrow is 80% of home value. Whereas, for commercial mortgage, 70% of property value is the maximum limit.

Available amount can be differ from your down payment, financial conditions, creditworthiness etc.

Learn more about how much you can borrower with Residential mortgages Calculator

Down Payment is the amount used to purchase a real estate which comes out of your own saving. If you can afford to pay more down payment, you can decrease your loan amount.

For example, in case you buy new house priced CAD$ 500,000 and if you pay 30% (CAD$ 150,000) down payment , your mortgage loan amount would be CA$350,000.

If your down payment is less than 20% of total amount, mortgage insurance is required. This is legal requirement by Government of Canada and the purpose of mortgage insurance is to protect financial institution (lender) in case borrowers are not able to make mortgage payment.

Mortgage insurance allow you to purchase real estate with less down payment but certain percentage of premium will be added as an additional cost. Premium will vary depending on your mortgage condition (amount, amortization period and down payment amount etc.)

Mortgage can be divided into two kinds; ‘Insured Mortgage’ and ‘Uninsured mortgage’. Shinhan Bank Canada is offering ‘Uninsured Mortgage’ only.

Term for mortgage is the length of period the borrower must commit to the mortgage rate and conditions with the lender. you either have to pay off remaining balance or renew with another term when the existing term ends.

At Shinhan Bank Canada, terms range from 1 to 5 years.

There are two types of term for a mortgage;

- Closed Term: You can only prepay a limited amount of principal without paying prepayment penalty. The mortgage rate for a closed term is generally lower than the rate for an open term mortgage.

- Open Term: You can make a partial or full repayment anytime without paying prepayment penalty. However, the mortgage rate for an open term mortgage is generally higher than the rate for a closed term mortgage.

Amortization Period is the total life of the mortgage. At the end of the amortization period, the mortgage is expected to be paid in full.

The maximum amortization period permitted for residential mortgages and commercial mortgages are as below;

- Residential Mortgage up to 30 Yrs

- Commercial Mortgage up to 25 Yrs

Longer amortization period means you will be paying lower monthly / bi-weekly payments, but you will pay more in interest over the life of the loan as it takes longer to fully payoff the mortgage.

There are two main payment methods for a mortgage at Shinhan Bank Canada:

- Fixed payment : You will pay fixed amount on every payment schedule, but the principal and interest portion paid will be different within the fixed amount. The principal repayment portion will gradually increase as long as the interest rate remains constant.

- Variable Payment (for variable Rate loans only): You will be paying fixed amount of principal and accrued interest on their regular payments. Regular payment amount will differ each payment, but the amount of principal repaid will be constant throughout the term. Total interest to be paid at the end of the amortization period will be the less compared to the other payment method, as the interest amount will lower due to faster principal reduction at earlier stage of the loan.

Payment can be made either Monthly or Bi-Weekly .

If you would like to pay off your mortgage faster, there are ways you may consider:

1. Change in regular payment frequency/method/amount

You can request to increase your payment frequency, your regular payment amount or change the payment method to pay down your mortgage faster.

2. Prepayment

A prepayment (also known as lump-sum payment) is when a borrower wishes to pay down a mortgage partially or in full before the end of the term. Prepayment penalty will be charged if you make a payment toward your principal beyond prepayment privilege. For closed term mortgages, Shinhan Bank Canada lets the borrowers to make a prepayment up to 10% of the outstanding balance annually without a penalty (based on anniversary date, not calendar date).

Please contact our branch for more information.

Branch Info: https://www.shinhan.ca/about-us/find-us/branch-info/

[Prepayment penalty Calculation]

Variable Interest Rate Mortgage: Equal to 3 months of interest of the remaining balance.

Fixed Interest Rate Mortgage: Higher of the following:

– 3 months of interest

– IRD (Interest Rate Differential) which is determined by Posted rate for the agreed term and current posted rate for the remaining term.

Refer to your Cost of Borrowing Disclosure Statement for more detail on how prepayment penalty is calculated, or use Mortgage Prepayment Penalty Calculator to see approximately how much your prepayment penalty will be.

It is the policy of the Bank to charge an equitable interest rate to the borrowers with the amount of risk involved in a credit transaction and the amount of services provided.

The Bank is entitled to a fair interest rate and will come up with sincere services and reasonable conditions to its customers in return.

We can provide you professional advices and our competitive rates.

Please refer to the link below for more detailed information.

Branch Info: https://www.shinhan.ca/about-us/find-us/branch-info/

Mortgage Rate: https://www.shinhan.ca/loans/mortgages/mortgages-interest-rate/

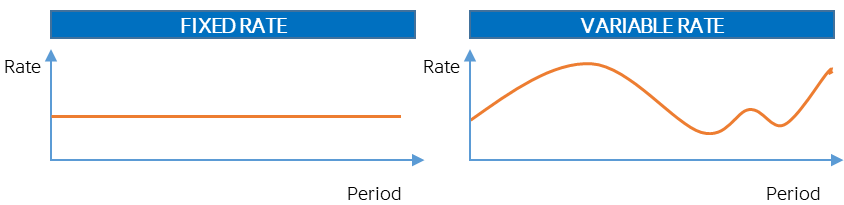

There are two types of Interest Rate, which is Fixed Rate and Variable Rate upon agreement.

- Fixed Interest Rate: Interest rate and regular payments will stay the same until the end of the term. You won’t have to worry about rate fluctuations as your rate will be protected.

- Variable Interest Rate: Interest rate may fluctuate according to changes in prime rate. Variable Rate is determined as Prime rate plus Spread. Spread will not change during the mortgage term, but Prime rate may. Your payment will be paid more toward interest if the prime rate increases. On the other hand, your payment will be paid more towards principal if the prime rate goes down.

You can find Shinhan Bank Canada’s Prime Rate at: https://www.shinhan.ca/loans/mortgages/mortgages-interest-rate/